How I Spotted the Turn Before My Business Failed – A Strategy That Saved Me

I never thought my business would collapse. One day it was thriving; the next, I was drowning in debt and bad decisions. But in that chaos, I learned something powerful: trend judgment isn’t just for traders—it’s survival for entrepreneurs. I started watching signals I’d once ignored. This is how I rebuilt—not by luck, but by strategy. If you’re feeling the ground shift, this could be what saves you too. The warning signs were there all along—slower customer responses, shrinking margins, rising costs masked by volume. I mistook momentum for security. When the downturn hit, it wasn’t sudden. It was the result of months of ignored signals. This story isn’t about failure. It’s about what comes after—the clarity, the discipline, and the quiet confidence that comes from learning how to see before you fall.

The Breaking Point: When Success Suddenly Crumbled

It began with a quiet unease. Orders that once arrived steadily started arriving late. Clients who used to renew without hesitation now asked for extensions, discounts, or paused altogether. At first, I told myself it was seasonal. A blip. Every business has slow months. But the numbers didn’t bounce back. Cash flow, once predictable, became erratic. Bills stacked up while receivables lagged. I found myself dipping into personal savings just to cover payroll. The emotional weight was just as heavy. I had built this company from scratch—late nights, skipped vacations, reinvested profits. It wasn’t just a business; it was my identity. Watching it unravel triggered a mix of denial, shame, and panic. I kept hoping things would turn around on their own, that one big client would save us. But hope isn’t a strategy.

The real breaking point came six months in, when I realized we had lost three major accounts within eight weeks—not due to poor service, but because their own industries were contracting. I hadn’t noticed the broader economic shift. I was too focused on operations to see the environment changing around me. My mistake wasn’t poor execution; it was poor observation. I had confused activity with progress. We were still busy—responding to emails, fulfilling smaller orders, managing logistics—but we weren’t growing. We were surviving on fumes. By the time I acknowledged the crisis, we were already months behind the curve. The lesson was brutal but clear: success doesn’t protect you from decline. In fact, past success can blind you to danger. The most dangerous moment in business isn’t failure—it’s the illusion of stability when everything is quietly falling apart.

Seeing the Signals: What Trends I Missed (And Shouldn’t Have)

In hindsight, the warning signs were unmistakable. The first was customer behavior. Clients began asking more questions about pricing, requesting longer payment terms, and showing less urgency in decision-making. These weren’t isolated incidents—they were patterns. I dismissed them as negotiation tactics or individual concerns, but they were actually reflections of broader financial caution in the market. When multiple customers start acting the same way, it’s not coincidence; it’s a signal. I failed to connect the dots because I was too close to the day-to-day operations. I treated each interaction as a standalone event rather than part of a larger trend. What I didn’t realize was that customer sentiment is one of the earliest and most reliable indicators of economic shifts. When confidence drops, buying habits change—slowly at first, then all at once.

Another critical signal was the lengthening of the sales cycle. Deals that used to close in four to six weeks began stretching to ten, twelve, even fourteen weeks. I blamed internal inefficiencies—maybe our proposals weren’t strong enough, or our follow-ups weren’t timely. But the issue wasn’t us; it was the market. Decision-makers were taking longer because they were under pressure to justify every expense. Budget approvals required more layers of review. The hesitation wasn’t about our value—it was about their risk tolerance. At the same time, operational costs were creeping up. Supplier prices increased, delivery times slowed, and staffing became more expensive due to rising minimum wages and turnover. We absorbed these costs to maintain margins, but that only delayed the inevitable. Volume masked the problem until it couldn’t. The combination of shrinking revenue and rising costs created a silent squeeze—one I didn’t see until it was too late.

Perhaps the most telling sign was internal morale. As uncertainty grew, so did anxiety among the team. Good employees started looking elsewhere. Retention became a challenge. I interpreted this as a leadership issue, but it was also a market signal. When talent begins to leave, it’s often because they sense instability before leadership does. Employees are close to the work and feel the strain of declining resources, missed targets, and shifting priorities. Their instincts are worth paying attention to. I had treated these signs as operational problems to be managed, not strategic warnings to be heeded. The truth is, every aspect of a business—from customer interactions to employee sentiment—carries information. The key is learning how to read it before it becomes a crisis.

From Reaction to Strategy: Building a Trend-Watching Mindset

The shift from crisis management to strategic foresight didn’t happen overnight. It required a fundamental change in how I approached decision-making. For years, I had operated in reactive mode—putting out fires, chasing deadlines, celebrating short-term wins. That worked during growth periods, but it left me vulnerable when conditions changed. The turning point came when I realized that survival depended not on working harder, but on thinking differently. I needed to move from being a problem-solver to a pattern-seeker. This meant stepping back from daily operations and creating space to observe, analyze, and anticipate. It wasn’t easy. Letting go of control felt risky, but staying stuck in reaction mode was riskier.

I started by setting aside dedicated time each week—just two hours—for reflection and review. No emails, no meetings, no distractions. During this time, I reviewed financial reports, customer feedback, industry news, and internal performance metrics. The goal wasn’t to fix anything immediately, but to notice patterns. Were certain products selling less? Were clients from a particular region pulling back? Was employee turnover higher in one department? I began to see connections I had missed before. For example, I noticed that clients in the manufacturing sector were slower to renew, while those in healthcare remained stable. That wasn’t random—it reflected broader economic trends. Manufacturing was facing supply chain disruptions, while healthcare demand remained resilient. This kind of insight couldn’t be gained in a crisis meeting. It required calm, consistent observation.

Another critical part of the mindset shift was learning to prioritize data over emotion. When the business was failing, every decision felt urgent and personal. I made choices based on fear, hope, or loyalty—not logic. To counter this, I established simple rules: no major decision without reviewing at least three data points. This forced me to slow down and seek evidence before acting. It also reduced the influence of bias. For instance, I once wanted to invest in a new marketing campaign because I believed in the product. But the data showed declining engagement and customer acquisition costs rising. Without that check, I might have wasted precious resources. The trend-watching mindset isn’t about predicting the future perfectly—it’s about reducing uncertainty through disciplined observation. It’s about building a habit of asking, “What am I seeing?” instead of “What do I want to see?”

The Early Warning Framework: A Practical System Anyone Can Use

From my experience, I developed a simple but effective early warning system—one that doesn’t require expensive software or advanced analytics. It’s built on three core components: key indicators, regular review, and threshold triggers. The first step is identifying the vital signs of your business. These vary by industry, but common ones include monthly revenue trends, average customer lifetime value, payment delays, employee turnover rate, and supplier cost changes. Choose four to six metrics that directly reflect your financial health and customer demand. Track them weekly or monthly in a simple spreadsheet. The goal isn’t complexity—it’s consistency. Seeing the data over time reveals patterns that aren’t visible in isolated reports.

The second component is benchmarking. It’s not enough to know your numbers—you need context. How do your sales trends compare to industry averages? Are your competitors facing similar challenges, or is the issue internal? Public data, trade associations, and market reports can provide valuable reference points. For example, if your revenue drops 15% in a quarter, that’s concerning. But if the entire sector is down 20%, your performance might actually be strong. Conversely, if you’re the only one struggling, the problem may lie in your operations or positioning. Benchmarking helps distinguish between market-wide shifts and company-specific issues. It prevents overreaction and guides more accurate responses.

The third part of the system is setting threshold triggers—specific levels at which action is required. For instance, if customer renewals fall below 70% for two consecutive months, that triggers a review of service quality and client feedback. If cash reserves drop below three months of operating expenses, it triggers cost assessments and liquidity planning. These thresholds turn observation into action. They remove emotion from decision-making by creating predefined responses to specific conditions. The system doesn’t guarantee perfect foresight, but it creates a structured way to detect trouble early. It turns vague concerns into concrete signals. And most importantly, it gives you time—time to adjust, adapt, and act before a dip becomes a collapse.

Risk Control in Crisis: Protecting What’s Left When Failure Hits

Even with early warnings, some downturns are unavoidable. When the decline is confirmed, the focus must shift from growth to preservation. The goal is no longer expansion—it’s survival with options. This requires disciplined risk control. The first priority is liquidity. Cash is oxygen in a crisis. I began by conducting a full financial triage: listing all incoming and outgoing funds, identifying non-essential expenses, and prioritizing obligations. Some costs had to be cut immediately—luxury software subscriptions, non-revenue-generating staff roles, unused office space. It was painful, especially when it meant letting people go, but preserving cash was essential to keep the business alive. I also renegotiated payment terms with suppliers and landlords, asking for deferrals or reduced rates. Many were willing to work with me when I approached them honestly and proactively.

At the same time, I protected core capabilities. Not all cuts are equal. I avoided slashing areas that would prevent recovery—such as customer support, product development, or key relationships. The idea wasn’t to shrink at any cost, but to streamline strategically. I also paused new investments and focused on maximizing returns from existing assets. For example, instead of launching a new product line, I doubled down on our best-selling items and improved their profitability. I reviewed pricing models and adjusted them based on demand elasticity—raising prices for high-demand services while offering limited-time promotions to clear slow-moving inventory. Every decision was evaluated through the lens of cash flow impact and long-term viability.

Emotional discipline was just as important as financial discipline. In crisis, it’s easy to make impulsive decisions—either freezing completely or swinging wildly between extremes. I committed to a decision-making framework: assess the data, consult trusted advisors, wait 24 hours before acting on major choices. This simple rule prevented panic-driven mistakes. I also communicated openly with my remaining team, explaining the situation and our plan. Transparency built trust and kept morale from collapsing. Risk control isn’t about avoiding loss—it’s about managing it wisely. The goal is to emerge from the crisis with enough stability to rebuild, not just survive.

Turning Collapse Into Clarity: How I Rebuilt with Smarter Moves

Stabilization was only the beginning. The real work came in rebuilding—not as a return to the old model, but as a redesign based on what I had learned. I used the trend-judgment skills I had developed to inform every decision. First, I reevaluated our customer base. Instead of serving everyone, I focused on the segments that were still growing and showed loyalty. I analyzed data to identify who was still buying, who paid on time, and who referred others. These became our priority clients. I tailored offerings to their needs, improving service and deepening relationships. At the same time, I phased out clients who were high-maintenance, late-paying, or declining in volume. It was counterintuitive—letting go of revenue—but it improved profitability and reduced stress.

Pricing strategy also changed. I moved away from discounting as a default tactic. Instead, I implemented value-based pricing, where fees reflected the actual benefit delivered. This required better communication and stronger client education, but it resulted in higher margins and more sustainable revenue. I also diversified income streams, adding subscription-based services that provided predictable monthly income. This reduced reliance on one-time projects and smoothed cash flow. Marketing shifted from broad outreach to targeted engagement—using email campaigns, referral programs, and content that spoke directly to our ideal clients. Every dollar spent on promotion was measured for return.

Perhaps the most important change was in timing. I learned to act earlier. When I saw a slight dip in engagement, I investigated immediately instead of waiting. When a supplier raised prices, I explored alternatives right away. This proactive stance prevented small issues from becoming big problems. Rebuilding wasn’t faster than the original growth—it was smarter. It wasn’t driven by hustle, but by insight. And because it was aligned with actual market demand, not wishful thinking, it was more resilient. Within two years, we weren’t just back—we were stronger, leaner, and more focused than before.

Lessons Beyond Survival: Why Trend Judgment Is the Ultimate Financial Shield

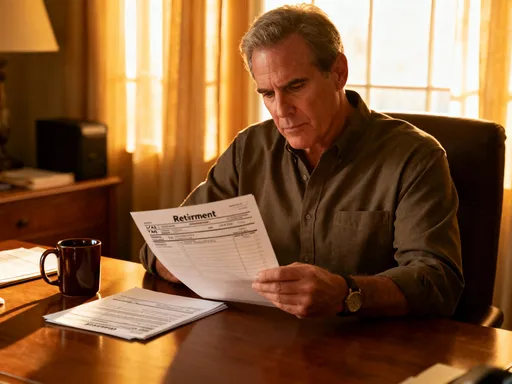

The experience taught me that financial resilience isn’t about having the most money or the biggest team—it’s about having the clearest vision. Trend judgment is the skill that turns uncertainty into advantage. It’s not about making bold predictions; it’s about noticing small changes before they become large disruptions. It’s the difference between steering and drifting. In personal finance, the same principles apply. Monitoring your spending patterns, recognizing changes in income stability, and adjusting habits early can prevent financial crisis. Whether you’re running a business or managing a household budget, the ability to see trends is a form of power. It allows you to act with confidence, even when conditions are unclear.

What I once saw as a personal failure became a professional transformation. The collapse didn’t break me—it sharpened me. It taught me that awareness is the first line of defense, discipline is the foundation of recovery, and adaptability is the key to longevity. These aren’t just business lessons—they’re life lessons. For anyone feeling the pressure of change, whether in work, income, or daily expenses, the message is this: pay attention. Look beyond the noise. Track your numbers. Listen to the signals. Survival isn’t luck. It’s the result of learning how to see—before the fall, during the storm, and on the way back up. That’s not just strategy. That’s financial wisdom.